Whenever you find yourself on the side of the majority, it is time To Reform. - Mark Twain

The Sequence of Returns Problem: Why the Order of Your Losses Matters More Than the Size of Them

Most people spend their financial life focused on the wrong number.

They track their average annual return. They celebrate when the market is up. They tell themselves the long-term average is what matters. And for a long time — during the accumulation phase — they are mostly right.

But retirement changes the math in a way most people never see coming.

In retirement, your average return does not tell you whether you will run out of money. The order of those returns does.

The Concept Wall Street Doesn't Lead With

Average return is a useful number when you are not taking withdrawals. If two portfolios both average 8% over 25 years, and you never touch the principal, they end up in the same place — regardless of whether the gains came early or late.

That changes the moment you start drawing income.

When you take withdrawals from a portfolio during down years, you are selling assets at a loss to fund living expenses. Those shares — or units — are gone. They cannot recover when the market comes back. You have permanently reduced your base.

This is called sequence of returns risk, and it is the single most underexplained threat to retirement income in mainstream financial planning.

The Same Returns. Completely Different Outcomes.

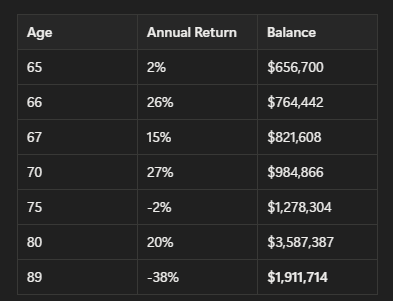

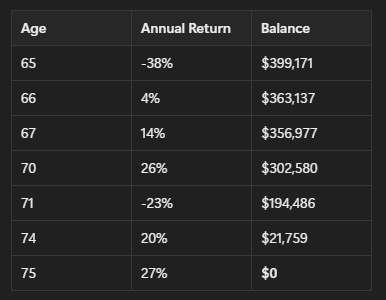

Here is a hypothetical comparison. Two portfolios. Both start at $693,824 at retirement. Both take $50,000 in annual income withdrawals. Both have the same average annual return over time.

The only difference: the order of the returns is reversed.

Portfolio A — Favorable Sequence (strong returns early):

Portfolio B — Unfavorable Sequence (losses early):

Portfolio A ends with nearly $1.9 million. Portfolio B runs out of money completely by age 75 — twenty years before Portfolio A winds down.

Same average return. Same starting balance. Same withdrawal amount.

One funds a comfortable 25-year retirement and leaves a legacy. The other is empty in ten years.

Why This Happens

The math is straightforward once you see it.

When a portfolio drops 30% and you withdraw $50,000 on top of that loss, two things happen simultaneously: your balance shrinks from the market decline, and your balance shrinks from the withdrawal. When the market eventually recovers, it is recovering a much smaller base — one permanently reduced by every dollar you spent during the downturn.

Early losses are disproportionately damaging not because they are bigger, but because you have fewer assets to recover with, and more years of withdrawals ahead of you.

Early gains do the opposite — they let your full balance compound before losses arrive, building a cushion large enough to absorb them.

The problem is that no one gets to choose which sequence they retire into. You get the market you get. The S&P 500 experiences a down year roughly three out of every ten years. Retiring into one of those years is not bad luck. It is a statistical certainty for a meaningful portion of retirees.

The Fix Is Not About Picking Better Stocks

The conventional response to sequence of returns risk is some version of "hold a more conservative allocation as you approach retirement." Move from equities to bonds. Reduce volatility. Accept lower returns in exchange for stability.

That is one approach. It is not the only one, and it is not the most powerful one.

The more effective solution, supported by the same Penn Mutual research, is this: have other sources of income available to pull from during down years, so you never have to sell portfolio assets when they are at a loss.

When you avoid withdrawals from your investment portfolio in negative return years — by drawing income from an alternative source — your portfolio retains its full recovery potential.

Here is what that looks like using the same hypothetical framework. Market B scenario (losses early), with and without an alternate income source in down years:

Without alternate income in down years: CAGR = -4.22%

With alternate income used only in down years: CAGR = -0.24%

The difference in compound annual growth rate is nearly 4 full percentage points — not from picking better investments, but from structuring when withdrawals occur.

That is the strategy. Not better returns. Better sequencing.

What That "Other Source" Can Look Like

This is where the concept connects to structure.

The whole life insurance cash value — the kind used in an Infinite Banking strategy — is a powerful tool for solving sequence of returns risk, and it is one of the most overlooked applications of permanent life insurance in retirement planning.

Here is why it works:

A properly structured whole life policy builds guaranteed, accessible cash value that is not tied to stock market performance. It does not decline in a bad market year. It does not require you to sell anything to access it. And unlike most retirement accounts, you can access the cash value through policy loans without triggering a taxable event or mandatory distribution rules.

This means in a year when your investment portfolio is down 20%, you can draw your living expenses from your policy's cash value instead. Your portfolio stays intact. It recovers on its full original base. And when markets come back, your sequence is no longer the enemy.

We covered the broader mechanics of borrowing against assets without triggering taxable events in Liquidity Without Liquidation. That article explains how different asset classes — real estate, securities lines, business equity, and whole life cash value — can all serve as liquidity sources that protect your portfolio from forced liquidation.

The whole life cash value is the version of that strategy specifically designed for retirement income sequencing.

📖 Related: The Diversification Lie Wall Street Sold You — sequence of returns is a layer-two risk. This article explains why traditional diversification does not protect against it, and what second-layer diversification actually requires.

The 4% Rule Problem

You may have heard of the 4% rule — the retirement guideline suggesting that withdrawing 4% of your portfolio annually is a sustainable withdrawal rate over a 30-year retirement.

The 4% rule was derived from historical data. It assumes a relatively stable sequence. It does not account for an unfavorable early sequence of returns.

Whether the 4% rule holds depends entirely on market performance — and specifically on when down years arrive. If the first five years of your retirement include a significant market decline, the 4% rule may fail even in scenarios where the long-run average return would technically support it.

This is not a fringe concern. It is the structural flaw in any withdrawal strategy built entirely on a single account with no alternative income source.

The Critical Thinking Three

Your financial plan likely shows a projected average annual return. Does it also show what happens to your retirement income if the worst three years come first — not last? The projection and the sequence are two completely different conversations.

If your only retirement income source is a portfolio that declines in down years, who benefits from that structure? The institutions managing your assets collect fees regardless of sequence. The risk of bad timing sits entirely with you.

What would it mean, practically, to have a cash value account you could draw from during market downturns — so your investment portfolio never has to be sold at a loss to fund your life? That is not a theoretical concept. It is a design decision, and it starts with building the right structure before you need it.

📬 Want one idea per week on building wealth outside the conventional system?

📞 Ready to explore how to structure a whole life policy as a retirement income buffer?

Related reading:

Liquidity Without Liquidation — how to access capital from your assets without selling them

The Diversification Lie Wall Street Sold You — why traditional diversification leaves one critical risk unaddressed

The "Free Money" Myth: What the IRS Actually Says About the 401(k) Match — the terms of your retirement account most people never read

Sources: Penn Mutual Life Insurance Company, "Sequence of Returns" (T4118, 2024) | Penn Mutual Advanced Sales, "The Importance of Diversifying Sources of Retirement Income" (PM9095, 2024) | S&P 500 Index historical return data via MarketWatch (November 2024)

Wealth And Liberty Newsletter

Get exclusive tips and updates

Copyright © 2026 Wealth And Liberty. All rights reserved.

Privacy Notice:

We respect your privacy. Your email address and personal information will never be sold, shared, or misused. Community participation and account registration are optional and exist only to support discussions and content interaction. Please review our Privacy Policy and Disclosures for full details.

Disclaimer :

Wealth & Liberty is an educational platform created to encourage thoughtful discussion around money, freedom, and long-term financial thinking. All information provided is for educational purposes only and should not be considered financial, legal, or investment advice. Any actions you take based on the content are your own responsibility. Always do your own research and consult qualified professionals before making financial decisions.