Liquidity without Liquidation

Liquidity without Liquidation

In 2022, Elon Musk pledged roughly $62.5 billion worth of Tesla shares to secure a $12.5 billion margin loan.

He used that loan to help acquire Twitter.

He did not sell a single Tesla share to do it.

That move — borrowing against an asset instead of selling it — is one of the oldest strategies in the wealth-building playbook. It just rarely gets explained to anyone outside of private banking offices.

This article is about that strategy. What it is, how it works across different asset types, where it breaks down, and which version of it offers the most structural advantages.

The Problem With Selling

Most people assume that accessing the value of an asset means selling it.

They need capital, so they sell stock. They hit a cash flow squeeze, so they liquidate a position. They want to fund a new opportunity, so they drain an account.

Every one of those moves triggers three things simultaneously.

First, a taxable event. Capital gains, depreciation recapture, ordinary income — the IRS collects the moment you convert an appreciating asset into cash. Depending on your bracket and holding period, that can mean handing 20–37% of your gain to the government before you spend a dollar.

Second, you permanently surrender future growth. Every dollar you liquidate stops compounding. It's not just the money you lose — it's every dollar that money would have become.

Third, you shrink your asset base. Wealth accumulates through asset ownership over time. Selling shrinks that base. Do it often enough and you're running in place.

The alternative is straightforward: instead of selling the asset to create liquidity, you borrow against it.

You access cash. The asset stays in place. The growth continues. And because you borrowed rather than sold, there is no taxable event. A loan is not income. The IRS does not treat a loan as a realized gain.

The Only 3 Ways to Transact

Every time you spend money — whether you are buying a liability like a car or acquiring an asset like real estate — the transaction happens one of three ways. That's it. There is no fourth option.

It doesn't matter if the purchase is $5,000 or $5 million. It doesn't matter if it's a depreciating liability or an appreciating asset. The mechanics of how you fund that transaction fall into one of these three patterns. And the pattern you choose determines whether wealth accumulates, stagnates, or quietly drains away over time.

Most people cycle between the first two their entire lives without realizing the third exists.

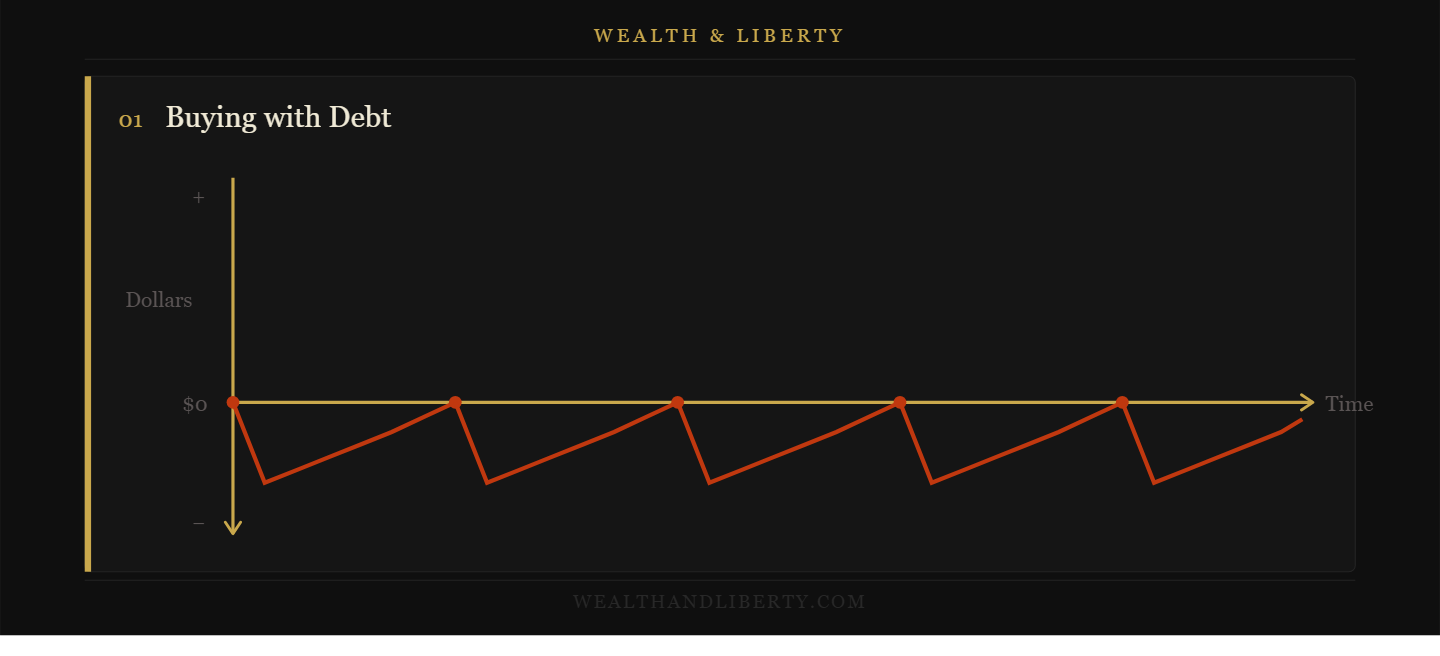

Buying with Debt

You need capital — a car, equipment, a renovation — and you go to a bank. If your credit score is acceptable, the bank lends the money under its terms: origination fees, a fixed repayment schedule, a lien against the asset. You pay interest to the bank, pay off the loan, return to zero — and then repeat the cycle for the next purchase.

Every cycle starts at zero and ends at zero. The bank captures the interest. Your wealth does not grow.

Buying with Debt: Borrow → Pay Interest to Bank → Return to Zero → Repeat

Chart 1: Each purchase cycle starts at $0, dips below zero as the loan is taken and interest accumulates, then slowly climbs back to $0 as the debt is repaid. The bank captures the interest. Net wealth never advances — every cycle resets.

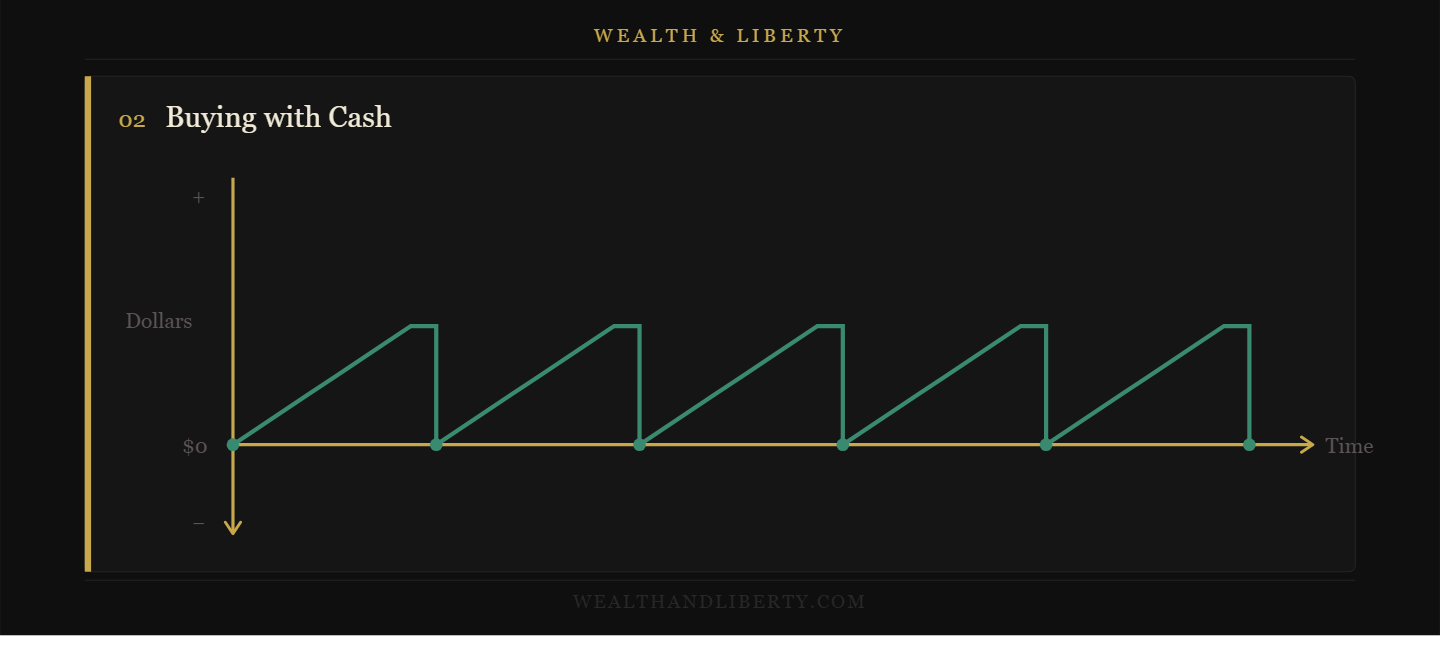

Buying with Cash

You avoid debt by accumulating cash before making purchases. No loan interest accrues — which looks like an improvement. But to maintain liquidity, savings typically sit in low-yield accounts not designed for growth. When the purchase is made, the savings are depleted back to zero. Then the savings cycle begins again.

You also return to zero at the end of each cycle. No interest paid to a bank — but no wealth accumulation either. The capital is consumed by every major purchase.

Buying with Cash: Save → Spend → Return to Zero → Repeat

Chart 2: Savings accumulate above $0 in a staircase pattern, then drop vertically back to zero at each purchase. No interest paid to a bank — but principal is fully consumed every cycle. No compounding because the base is removed with every transaction.

As the book Financial Independence in the 21st Century notes: neither the cash buyer nor the debt buyer comes out ahead on major capital purchases. There is another way.

Buying with Asset-Collateralized Debt

Instead of borrowing from a bank or depleting savings, you borrow against an asset you already own. The asset stays in place. The loan comes from the asset's collateral value — not from selling it.

Here is the critical difference: the asset continues to compound and grow while the loan is outstanding. You are not withdrawing money — you are borrowing against it. So the asset's growth is uninterrupted.

When the loan is repaid, the full asset value is restored. And unlike the debt buyer or cash buyer, you do not return to zero at the end of each purchase cycle. Wealth accumulates throughout.

Buying with Asset-Collateralized Debt: Borrow Against Asset → Purchase → Repay on Own Schedule → Asset Grows Throughout → Repeat at a Higher Base

Chart 3: Two lines move upward together over time. The dotted line is the asset's uninterrupted contractual growth — it never dips. The solid line tracks alongside it, briefly separating below at each purchase (the loan), then climbing back up to rejoin. Each cycle starts from a higher floor. Wealth compounds continuously, even while borrowing.

Buying with debt returns you to zero. Buying with cash returns you to zero. Buying with asset-collateralized debt — the right kind, structured correctly — is the only pattern where your base grows with every transaction.

"But I Still Pay Interest"

Yes. You do.

This is the first objection — and it's a fair one. Borrowing against an asset isn't free. You pay interest on the loan. So why is this better than just saving up and paying cash?

Because the interest you pay is only part of the equation. The other part is what your underlying asset earns while the loan is outstanding. As long as your asset is growing at a higher rate — or on a significantly larger base — the interest you pay will be less than the wealth your asset generates over the same period. Additionally scale this out to a lifetime, scale it out to a multigenerational strategy. This is where it becomes extremely powerful because your underlying asset(s) are always compounding without being interrupted.

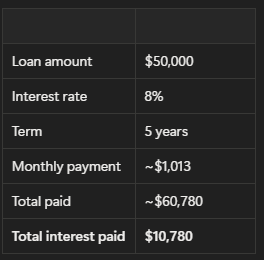

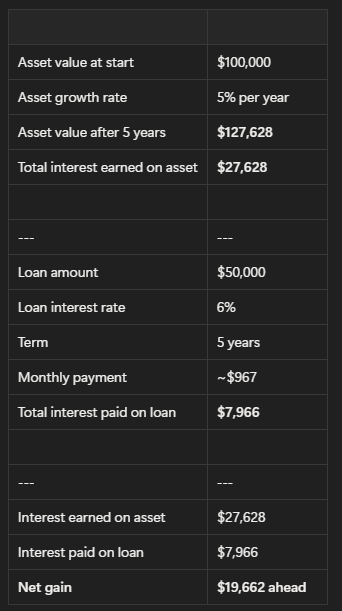

Let's make this concrete with a $100,000 asset and a $50,000 purchase.

Scenario 1: Buying with Debt (no asset, just a loan)

You don't have the equity to support the purchase — you're starting from zero and taking on $50,000 in debt at 8% interest over 5 years.

You paid $10,780 to a lender for the privilege of accessing capital you didn't have. At the end of 5 years you're back to zero — and the lender captured every dollar of that interest. No asset grew. Nothing compounded. The purchase simply cost you $10,780 more than the sticker price.

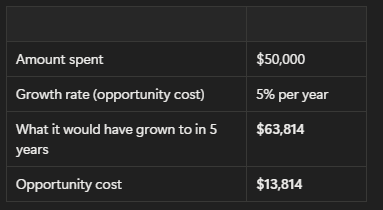

Scenario 2: Buying with Cash (depleting savings)

You have $100,000 saved. Some financial influencers will tell you to use it — avoid debt, pay cash, stay clean. So you spend $50,000 on the purchase. Smart move?

Not quite. Here's what that $50,000 would have become if you'd left it alone:

You paid no interest to a bank — but you silently surrendered $13,814 in growth. Your $100,000 is now $50,000. To rebuild back to $100,000 in 5 years at 5%, you'd need to save an additional ~$580 per month on top of your remaining $50,000 compounding.

At the end of 5 years you're approximately back where you started — with nothing to show for the growth that should have compounded during that window. The purchase didn't just cost you $50,000. It cost you $50,000 plus five years of lost momentum.

Scenario 3: Buying with Asset-Collateralized Debt

You have a $100,000 asset growing at 5% per year. You take a $50,000 loan against it at 6% interest over 5 years. Since you have collateral, you can usually get more favorable interest rates. The asset never stops compounding.

The chart above shows all three scenarios side by side. Notice the bottom panel: even when your asset earns the exact same rate as your loan charges, you still come out ahead — because you are earning on $100,000 but only paying interest on $50,000. Same rate. Different base. That difference is the arithmetic of asset-collateralized borrowing.

You made the same $50,000 purchase. You paid interest — $7,966 of it. But your asset generated $27,628 while the loan was outstanding. It was compounding at a higher basis than if you would have liqudated it to $50,000 and paid $50,000 in cash. You come out $19,662 ahead compared to having done nothing, and the purchase was still made.

Compared to the debt buyer: you paid $2,814 less in interest and your asset grew.

Compared to the cash buyer: you avoided $13,814 in opportunity cost and still have your full asset base intact. You did not trigger any taxes or lose out on the full asset growth.

The interest you pay on a collateralized loan is a cost. But it is a cost measured against a growing asset — and when the asset's growth exceeds the loan's cost, borrowing is not a burden. It's arithmetic.

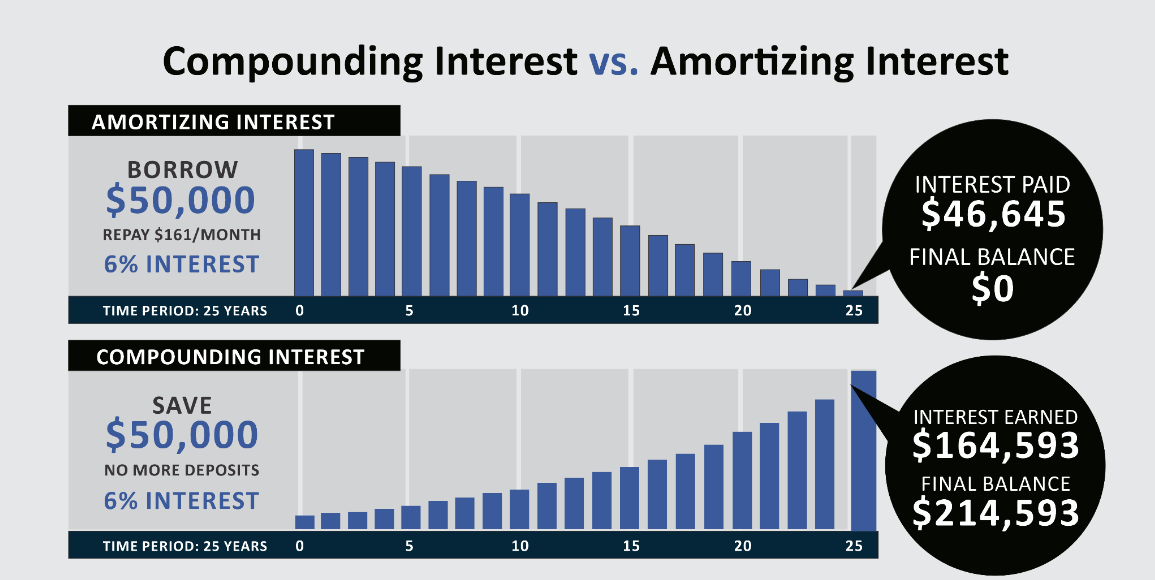

BUT What if your asset growth is the same or less than the interest rate on the loan?

That is a fair question and from the surface level it would appear to be a wash loan (0 cost) OR it could still have a negative interest cost. What is needed to analyze is time. When you take on a loan, you are usually paying amortized interest meaning the interest is recalculated on a declining balance. Conversely, the interest earned is earning interest on a higher basis. Over time these two interest forces work in your favor.

The question now becomes; would you pay $46,645 to earn $164,593?

The Toolbox: Ways to Borrow Without Selling

Not all collateral is equal, and not all borrowing structures carry the same risks. Here are some examples.

Securities-backed lines of credit (SBLOCs)

A securities-backed line of credit uses a brokerage portfolio — stocks, bonds, funds — as collateral. You keep the portfolio invested and draw cash against it as needed.

Typical advance rates run 50–70% of the portfolio's value for diversified, high-quality holdings. Concentrated single-stock positions get lower rates — Musk's Twitter margin loan reportedly used roughly a 20% loan-to-value ratio on his Tesla position.

The math can be compelling. One Nationwide analysis found that borrowing $40,000 against an appreciated portfolio through an SBLOC — rather than liquidating — could leave an investor with roughly $400,000 more in cumulative wealth over ten years, even after paying approximately $156,000 in interest. The reason: avoiding a ~$323,000 upfront tax bill and keeping the full portfolio compounding throughout.

The risk: if the portfolio falls in value, the lender can issue a margin call — demanding additional collateral or immediate repayment. This is exactly what happened to Musk when Tesla's share price dropped over 40% from the deal reference price, reportedly triggering a margin call on the facility. Liquidity without liquidation at billionaire scale — highly efficient, and highly fragile when the collateral is volatile.

Real estate equity

A cash-out refinance or home equity line of credit (HELOC) lets you extract equity from property without a sale. Typical LTVs run 60–80%.

Wealthier borrowers sometimes go further, pledging a securities portfolio as additional collateral to improve mortgage terms on a property purchase — keeping both the property exposure and the portfolio intact simultaneously.

The risk is tied to property values and rising interest rates on variable-rate structures.

Private business equity

Founders and business owners can borrow against the value of their companies through business lines of credit, SBA structures, or bespoke asset-backed loan arrangements.

The mechanics are less standardized than securities lending and require more lender diligence — but the concept is identical to what Musk did with Tesla, just at a different scale.

Collectibles, art, and luxury assets

High-value physical assets — fine art, rare watches, classic cars, wine collections, jewelry — can also serve as collateral through specialty lenders and art finance firms.

The mechanics work the same way: you retain ownership and continued appreciation potential while accessing a loan against the appraised value. Advance rates vary widely depending on the asset category, its liquidity, and the lender's appetite.

The key risk here is valuation. Unlike a publicly traded stock, the value of a Basquiat or a Patek Philippe is not updated in real time. Lenders apply conservative LTVs to account for that uncertainty, and forced liquidation of illiquid assets can result in prices well below market value.

Whole life insurance cash value

A properly structured whole life policy builds cash value that grows at a guaranteed contractual rate. That cash value is accessible through a policy loan — with no credit check, no approval process, and no lien on the purchased asset.

Critically, the cash value continues to grow while the loan is outstanding. You are not withdrawing from the policy — you are borrowing against it. This makes it structurally different from every other collateral type listed here. We'll explain exactly why in the section below.

The Tax and Compounding Math

The financial case for borrowing instead of selling comes down to two things: tax deferral and uninterrupted compounding.

Deferring a tax is not the same as avoiding one. But pushing a capital gains event into the future means the pre-tax amount keeps compounding — for years or decades — before the government collects. If the asset's return rate exceeds the loan's interest rate over time, you come out ahead even after paying interest.

The Nationwide case study puts numbers on this: in a high-bracket scenario, total interest cost on a ten-year SBLOC facility was still lower than the one-time tax hit from liquidating the same appreciated position. The investor who borrowed ended up approximately $166,000 ahead of the investor who sold — while preserving the full investment base throughout.

This is also why selling is more expensive than most people account for. It's not just the tax. It's the tax plus every dollar those after-tax proceeds would have earned if they had stayed invested. One interruption to compounding doesn't just cost you now — it costs you for decades.

We've covered this dynamic in our piece on Credit & The American Economy — the same structural math that makes consumer debt expensive is what makes premature liquidation expensive. The compounding runs against you the moment you interrupt it.

When This Works — and When It Doesn't

Liquidity without liquidation is not universally the right move. It depends entirely on the collateral and the borrower's situation.

It works well when the collateral is diversified, stable, and growing — when the borrower has income to service interest, a clear purpose for the capital, and a defined repayment plan. Whole life cash value, diversified brokerage portfolios, and real estate equity in stable markets all tend to hold their value as collateral.

It breaks down when the collateral is concentrated in a single volatile position, when borrowing is used speculatively, or when the borrower has no reliable cash flow to service interest. Musk's Twitter loan is the most prominent recent example of how a sophisticated structure still creates serious pressure when the underlying asset moves against you.

The discipline is the same as any use of leverage: you need to know your exit before you enter.

Why Whole Life Insurance Is in a Category of Its Own

Every collateral type covered above shares a common vulnerability: the collateral can fall in value, and when it does, the lender's terms change.

Whole life insurance operates on a different foundation entirely — and now that you understand the strategy, the distinction becomes clear.

A properly structured whole life policy builds cash value that grows at a guaranteed contractual rate, tax-deferred. That cash value is accessible through a policy loan — and here is the structural distinction that matters — borrowing against a whole life policy is generally a contractual right of the policy owner, not a discretionary lending decision by a bank.

Once the policy has sufficient cash value, no credit check is required. No loan committee reviews your application. No market price determines your eligibility. The right to borrow is written into the contract itself.

And critically: there is no margin call based on market volatility. (Unless you use some type of market based universal life product which is not recommended)

The structural risk profile is fundamentally different from pledging a stock portfolio. The cash value doesn't fall 5% in a day because of a news headline. The lender doesn't call the loan because your collateral dropped. The borrowing right is a contractual feature of the policy — not a discretionary banking decision

This is the only collateral structure where the asset is guaranteed to grow, the borrowing right is contractual, and the lender cannot change the terms based on market conditions.

This is why practitioners of the infinite banking concept use whole life insurance not primarily as a death benefit vehicle — though it provides that too — but as their own private capital system. A financing structure they control, not one a bank controls. It is a guaranteed asset to grow and has built in loan features that are superior to other lending institutions.

Want the full picture on how this works? Download our guide on Infinite Banking →

The Bigger Picture

Liquidity is not a cash problem. It's a structure problem.

Most people solve liquidity needs by cannibalizing their own wealth — selling assets to fund expenses, opportunities, or obligations. The alternative requires building an asset base that can generate liquidity on its own, without triggering the tax and compounding costs that come with a sale.

This connects to what we've written about the 401(k) as a capital control structure — a vehicle that locks your money away and dictates the terms of access. And to the employer match myth — the assumption that conventional savings vehicles automatically represent the best deal, without asking who controls the terms.

The through-line is always the same question: who controls the capital, and who controls the conditions under which you can access it?

Liquidity without liquidation is one answer. It's not the only one. But it's the one the system rarely explains to people who aren't already wealthy enough to have a private banker in their corner.

And it's worth being clear about the time horizon this strategy is designed for. This is not a one-time move. It is not a single clever transaction you execute once and walk away from. The families and institutions that use asset-collateralized borrowing most effectively treat it as a permanent operating system for capital — one they refine over decades and ultimately pass to the next generation. Every cycle compounds the base. Every loan repaid strengthens the asset. Every year the strategy runs, the gap between this approach and the conventional save-and-spend cycle widens. The real power is not in any single transaction. It is in never breaking the chain. Wealth transferred to the next generation with the structure intact — the assets, the borrowing rights, the compounding — means the next generation starts at a higher floor than you did. That is what multigenerational wealth actually means. Not a lump sum inheritance. A system.

The Critical Thinking Three

1. If borrowing against an asset can cost less than selling it — in taxes and lost compounding — why is selling treated as the default, and who profits when you sell?

2. Among the borrowing structures covered here — securities lines, real estate equity, business equity, whole life cash value — which one removes the lender's ability to change the terms when markets move? And why does that distinction matter?

3. If your current financial structure requires you to sell assets every time you need capital, is that a wealth-building strategy — or a system that keeps you permanently dependent on liquidation events?

Want to Go Deeper?

The Infinite Banking Concept is one of the most misunderstood — and most structurally sound — strategies available to business owners who want to control their own capital without depending on banks, markets, or the government's timeline.

📥 Download our full guide on Infinite Banking →

📅 Book a complimentary strategy call with our partners at Producers Wealth →

Wealth & Liberty publishes weekly on the financial decisions most advisors won't question. Subscribe to the newsletter →