Why the Most Regulated Institutions in America Hold Billions in Whole Life

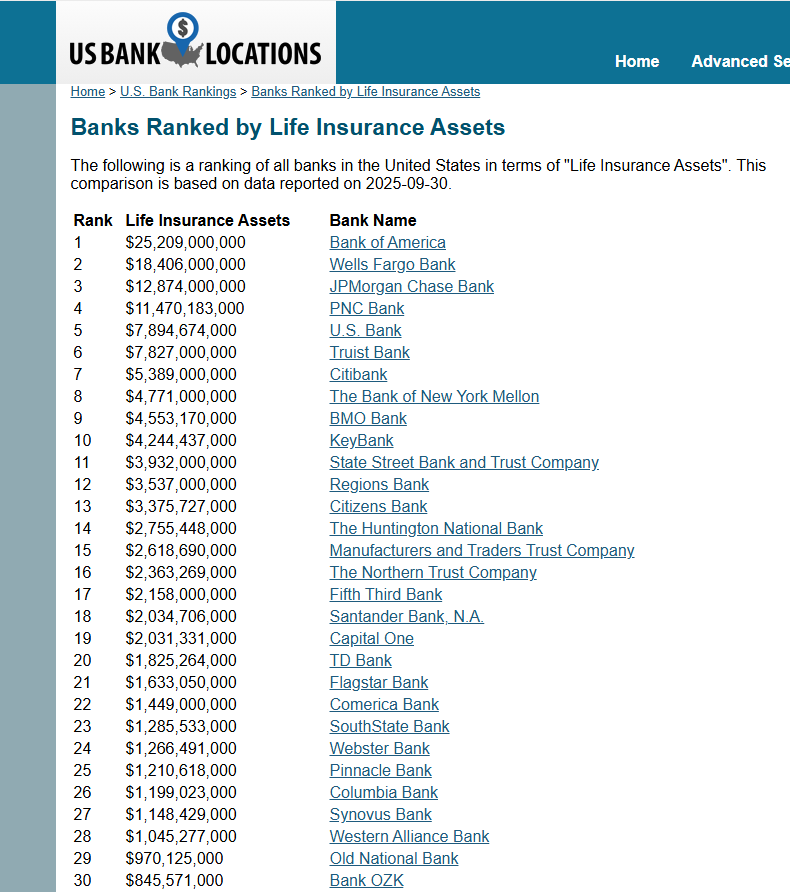

Bank of America holds over $25 billion in life insurance assets on its balance sheet.

Not in stocks. Not in real estate. Not in the kinds of assets your financial advisor has probably been recommending to you for years. In life insurance — specifically, in the cash value of whole life insurance policies held on the lives of their executives and key employees.

And Bank of America is not alone. Thousands of U.S. banks do this. The industry term is BOLI — Bank-Owned Life Insurance — and if you’ve never heard of it, that’s not an accident. It’s one of the quietest, most structurally sound capital strategies in American finance, and it has been hiding in plain sight on bank balance sheets for decades.

The chart below shows the top 30 U.S. banks ranked by life insurance assets. Study it for a moment before reading further.

Banks Ranked by Life Insurance Assets — U.S. Bank Locations

When you look at that chart, the question worth sitting with is not how much these banks hold in life insurance. The more important question is why.

Banks are not sentimental. They are not making emotional decisions. They are not buying life insurance because a salesman convinced them it was a good idea. These are the most heavily regulated, most scrutinized, most conservatively managed financial institutions in the world. Every dollar on their balance sheet is there for a reason. Every asset class they hold has been evaluated, stress-tested, and approved through layers of regulatory oversight and internal risk management.

So when thousands of banks, collectively holding tens — if not hundreds — of billions of dollars in life insurance assets, all arrive at the same conclusion independently, that is not coincidence. That is institutional wisdom. And it is worth understanding.

This article explains exactly why banks love life insurance, what it reveals about how they think about wealth, and what that means for the way you might think about your own.

A Brief History of BOLI — How Banks Got Here

Bank-Owned Life Insurance didn’t start as a grand strategy. It evolved out of a practical problem.

In the 1980s, banks were facing rising costs associated with employee benefit programs — particularly for executives. Pension obligations, deferred compensation plans, and post-retirement health benefits were creating long-term liabilities that needed to be funded. The question was: with what?

The IRS tax code offered an answer. Life insurance had long enjoyed favorable tax treatment — cash value grows tax-deferred, death benefits transfer income-tax-free — and banks began realizing that a properly structured whole life policy could serve as a pre-funding vehicle for these obligations. You pay a premium today, the cash value grows at a contractually guaranteed rate, and when the executive eventually dies, the tax-free death benefit reimburses the bank for the costs it incurred over the years.

Regulators took notice. In the 1990s and early 2000s, guidelines were formalized. The OCC (Office of the Comptroller of the Currency) and FDIC issued supervisory guidance defining how banks could hold BOLI, how much they could hold relative to tier 1 capital, and what due diligence was required. Rather than shutting the practice down, regulators essentially ratified it — acknowledging that when structured properly, BOLI was a sound, legitimate balance sheet asset.

Today, BOLI is a standard feature of institutional capital management. It is not fringe. It is not controversial. It is simply something that most individuals never learn about because it exists in the world of institutional finance, not personal finance.

That gap in knowledge is worth closing.

How Whole Life Insurance Actually Works as a Balance Sheet Asset

Before examining why banks use it, it helps to understand what they’re actually holding.

Whole life insurance — the type almost always used in BOLI strategies — is a permanent life insurance contract with two primary components: a death benefit and a cash value account.

The death benefit is straightforward. If the insured person dies, the bank receives a specified sum of money, income-tax-free, from the insurance company.

The cash value is less widely understood. From the moment premiums are paid, a portion builds inside the policy as guaranteed, contractually-defined cash value. This is not invested in the stock market. It does not fluctuate with interest rates in the way a bond does. It grows at a guaranteed minimum rate, plus dividends declared by the insurance company, and it has never gone backward in a dividend-paying whole life policy from a mutual insurance company.

For banks, this matters for several reasons. The cash value is an asset that can appear on the balance sheet at its current surrender value, which increases predictably over time. It does not mark to market the way equities or bonds do. It does not create earnings volatility. It does not require impairment charges during financial stress. It simply grows — quietly, contractually, and predictably.

This is not a return-maximizing asset. It was never designed to be. It is a stability asset — a foundation designed to support the structure above it without shifting underfoot.

With that foundation in place, here are the five reasons banks have allocated billions to it.

Reason 1: It Is One of the Most Tax-Efficient Assets the Tax Code Allows

Banks are not in the business of chasing returns. They are in the business of optimizing after-tax, risk-adjusted outcomes. Those are very different things.

BOLI offers a combination of tax advantages that is difficult to replicate with almost any other asset class:

Tax-deferred growth. The cash value inside a whole life policy grows without current taxation. A bank holding $100 million in BOLI cash value does not receive a tax bill each year as that value increases. The growth compounds on the full balance, uninterrupted. This is the same principle behind a 401(k) — except with no contribution limits, no market exposure, and no required distributions.

Tax-free death benefits. When an insured employee dies, the bank receives the death benefit income-tax-free under IRC Section 101(a). For large institutions funding executive deferred compensation, this tax-free reimbursement can be worth tens of millions of dollars over the life of the program.

Cost recovery for employee benefits. Banks use BOLI earnings to offset the cost of providing employee benefits. Because those earnings are not currently taxable, they effectively reduce the after-tax cost of the benefit programs the bank is already obligated to fund.

To put a number to what this means: if a bank is in a 25% effective corporate tax rate environment and holds an asset growing at 4% annually, the after-tax equivalent yield on a taxable asset would need to be over 5.3% just to match it. That gap compounds significantly over 10, 20, or 30 years.

Tax efficiency is not a footnote. It is, as the numbers show, a primary driver of long-term wealth accumulation. Banks understand this. Most individuals have never been taught to calculate it.

Reason 2: It Qualifies as a High-Quality, Stable Balance Sheet Asset

Under regulatory capital frameworks, not all assets are created equal. Banks must hold capital against risk-weighted assets, and the lower the risk weighting, the more efficiently that asset uses the bank’s capital.

BOLI — specifically the cash surrender value of whole life insurance — carries a favorable risk weighting under bank regulatory guidelines. The OCC has acknowledged its stability characteristics. It doesn’t gap down overnight. It doesn’t require a writedown when markets sell off. Its value is defined by a private contract with an insurance company, not by what someone is willing to pay for it on a given Tuesday.

Most BOLI is structured as a single-premium or limited-pay policy, meaning the bank makes a large upfront payment and the cash value is immediately positive. From day one, the asset on the balance sheet is worth something determinable and contractually guaranteed to grow.

Compare this to equities, where book value can collapse in weeks. Or to long-duration bonds, which can carry significant mark-to-market losses when interest rates rise — as we saw dramatically in 2022 and 2023 when rising rates devastated the bond portfolios of banks like Silicon Valley Bank, contributing directly to its collapse.

A bank that had allocated more of its capital to BOLI rather than long-duration treasuries would have been looking at steady, unremarkable cash value growth while its competitors were facing balance sheet crises. Boring, in this case, was survival.

The lesson is not subtle: assets that cannot collapse at the wrong moment preserve the ability to make decisions. That is not a small thing. That is the entire game.

Reason 3: It Perfectly Matches Long-Term Liabilities

One of the fundamental principles of sound financial management — whether for a bank, a pension fund, or an individual — is asset-liability matching. You fund long-term obligations with long-term assets. You do not fund a 30-year promise with a 90-day instrument.

Banks use BOLI specifically to fund long-tail liabilities: executive deferred compensation agreements, supplemental executive retirement plans (SERPs), post-retirement medical benefits, and split-dollar life insurance arrangements for key employees.

These are promises made today that will be paid out over decades. They need to be backed by an asset that will still be there — and will have grown — by the time those obligations come due.

Whole life insurance is purpose-built for exactly this profile. The cash value grows on a multi-decade curve. The death benefit provides a terminal backstop. The contractual guarantees remove the uncertainty of trying to time markets or project bond yields 25 years into the future.

A pension fund manager, asked how they plan to fund obligations due in 2045, does not point to a day-trading account. They point to long-duration, contractually certain instruments. BOLI is one of the most efficient of those instruments available to banks.

The principle translates directly to individuals. A business owner who has long-term obligations — funding a child’s education, replacing income in retirement, leaving a legacy to the next generation — benefits from the same matching logic. Long-term promises deserve long-term, contractually guaranteed assets behind them.

Reason 4: The Bank Owns and Controls the Asset Regardless of What Happens to the Employee

This is perhaps the most structurally revealing of the five reasons, and the one that most directly exposes the difference between institutional thinking and the way most individuals approach wealth.

In a BOLI arrangement, the bank is the policy owner and the beneficiary. The insured employee is named on the policy, but they own nothing. If that executive leaves the company, is terminated, retires, or even takes a competing job, the bank’s ownership of the policy does not change. The cash value keeps compounding. The death benefit remains intact. The asset stays.

Banks design their capital around assets they control — not assets that are subject to someone else’s decisions, timelines, or circumstances.

Contrast this with how most individuals hold wealth. Equity in a company can be diluted or lost if the business changes. A 401(k) is subject to government rules, tax law changes, and required minimum distributions on a timeline the individual did not choose. Real estate is illiquid and subject to market conditions at the precise moment you might need to access it. Even brokerage accounts are subject to capital gains events triggered by sales, dividends, and distributions that occur whether you want them to or not.

The bank’s approach — own the asset outright, control it contractually, retain it regardless of external circumstances — is a design philosophy, not just a tax strategy.

Ownership without control is exposure. Control without ownership is dependency. The combination of both, which is what a properly structured whole life policy provides to its owner, is what financial sovereignty actually looks like.

Reason 5: It Allows Banks to Arbitrage the Cost of Capital

Banks operate on spread. They borrow money from depositors at one rate and deploy that capital into assets yielding a higher rate. The difference is their margin, and managing that spread efficiently is the core of the banking business.

BOLI fits neatly into this model. When a bank’s cost of funds — what it pays depositors and bondholders to use their capital — is lower than the after-tax yield on a BOLI policy, the bank is earning a positive spread with essentially no credit risk, no market risk, and no liquidity event risk.

In environments where short-term rates are low, this spread can be significant. Even in higher-rate environments, the tax-equivalent yield on BOLI — accounting for the tax-deferred growth and tax-free death benefits — often remains competitive with taxable alternatives, especially for institutions in higher tax brackets.

More importantly, the certainty of the spread matters. A bank can model the cash value growth of a BOLI portfolio 20 years forward with a high degree of confidence. They cannot do that with equities. They cannot fully do it with bonds, which carry reinvestment risk and interest rate risk. But a whole life insurance contract, issued by a mutual insurance company with a 150-year track record of paying dividends, provides a reliable input into a long-range financial model.

Certainty of return, even at a modest rate, is worth more to an institution managing long-term liabilities than volatility of return at a higher average. Banks have learned this. It is baked into their capital allocation decisions at the highest levels.

What This Reveals About How Banks Actually Think

Step back from the five individual reasons and a coherent philosophy emerges.

Banks do not design their core capital around hope. They do not build their balance sheets around average returns or historical projections. They design around certainty, contractual guarantees, tax efficiency, and long-term control. They match assets to liabilities. They own what they deploy. They minimize leakage. They preserve optionality.

This is not a philosophy born of timidity. It is a philosophy born of experience — of watching what happens to institutions that do not practice it. The banks that have survived panics, recessions, regulatory upheaval, and rate cycles share a common trait: they built their foundations on assets that couldn’t be taken from them by market conditions.

Life insurance — specifically whole life — fits that description better than almost anything else in the tax code.

None of this is secret. The FDIC data is public. The OCC guidance is public. Bank balance sheets are publicly filed. The strategy is visible to anyone who looks.

The question is why this institutional wisdom has never filtered down to individual financial planning in a meaningful way. Why are individuals not taught to think about their personal balance sheet the way banks think about theirs? Why is the asset that Bank of America holds by the billions described as outdated or unnecessary when an individual considers it?

Those are questions worth sitting with. We explore the gap between what institutions do and what individuals are told to do throughout Wealth & Liberty. It is one of the central tensions this publication exists to examine.

If you want to understand how the same logic applies to your business and your personal balance sheet, that conversation starts with understanding what whole life insurance actually is — not what the industry has told you it is. You can explore that further with Producers Wealth, our life insurance partner, who works specifically with business owners thinking about these questions.

Related Reading

If this article raised questions about how these ideas connect to broader wealth strategy, the following articles go deeper on adjacent themes:

- The Legacy Waterfall: How the Ultra-Wealthy Transfer Wealth, Wisdom, and Control for 100 Years — How guaranteed assets function as the foundation of generational wealth transfer.

- The 401(k) Business Deal You Would Never Make — An examination of what the 401(k) actually looks like when evaluated as a business arrangement.

- The Hidden Inflation Hedge: How the Whole Life Death Benefit Outpaces the Dollar — The relationship between whole life insurance, monetary policy, and real purchasing power over time.

The Critical Thinking Three

Every article at Wealth & Liberty ends not with answers, but with questions. The goal is not to tell you what to think. The goal is to give you better tools for thinking.

- If the most conservative, regulated, and scrutinized capital allocators in the world have independently concluded that whole life insurance belongs on their balance sheet — what would it mean if that same logic applied to yours?

- When you evaluate financial decisions, are you comparing options on an after-tax basis — or are you comparing pre-tax numbers and missing the compounding difference that tax treatment creates over decades?

- The bank owns the policy, controls the asset, and retains it regardless of what happens to the employee. In your own financial life, how many of your assets do you own and control in that same unconditional sense?

Wealth & Liberty is an educational platform. Nothing in this article constitutes financial, legal, or tax advice. All content is for informational purposes only. Consult qualified professionals before making financial decisions.