A Nation of Speculators

Ask the average person what they own in their investment account and you’ll usually get some version of the same answer.

“I’m in the S&P 500.”

“I have a diversified portfolio.”

“I’m in a target-date fund.”

Ask them why — and the answers get thinner fast.

“Because that’s what you’re supposed to do.”

“Because it’s always gone up.”

“Because my advisor set it up.”

That’s not investing. That’s consensus-following dressed in investing language.

And the difference between the two isn’t academic. It’s the difference between a wealth plan that holds up under pressure and one that quietly reveals its fragility the moment conditions change.

What Investing Actually Requires

The word “investing” gets applied to almost everything done with money in public markets. It shouldn’t.

Genuine investing has a specific definition — one most retail participants never actually meet.

An investor allocates capital based on analysis of underlying value. They understand the business or asset they own. They can articulate the cash flows, the risk factors, the competitive dynamics, and the price at which the asset becomes compelling versus expensive. They have a view on what they’re buying, why it’s worth owning, and what would have to be true for it to be a mistake.

Most stock owners cannot do any of that for a single position in their portfolio.

They own the S&P 500 because it went up. They bought more when it kept going up. They held during drawdowns because they were told to stay the course. And they call it investing — because everyone else does too.

That’s not investing. That’s speculating on the continuation of a trend — with better marketing and a lower-cost ETF wrapper.

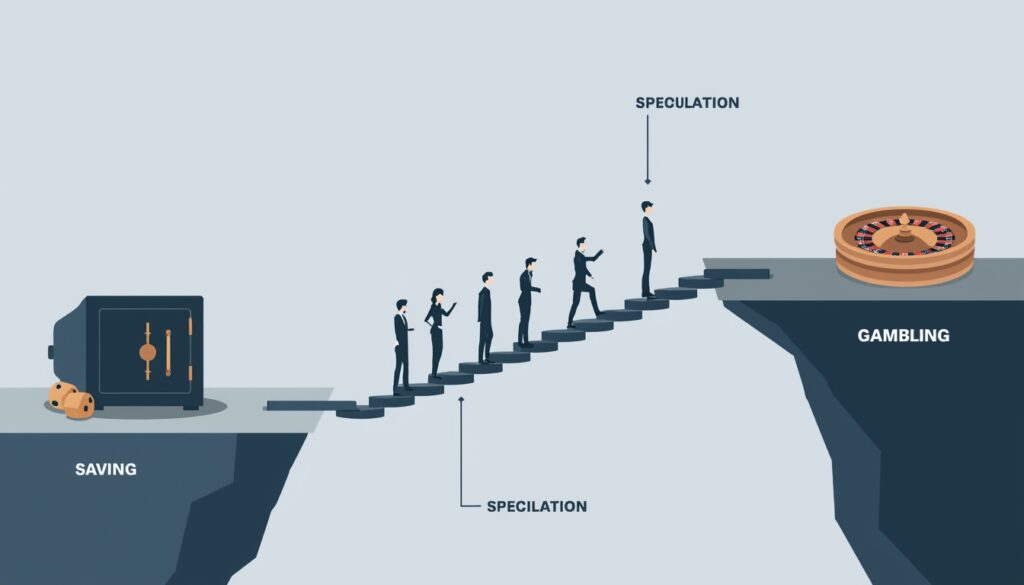

📖 Related: Compared to What? The Financial Spectrum No One Explains — The difference between saving, investing, speculating, and gambling isn’t the asset. It’s the purpose, the process, and what you actually understand about what you own.

The Spectrum Most People Have Never Mapped Their Money To

All capital sits somewhere on a spectrum from certainty to chance. Most people have never honestly placed their own portfolio on it.

Saving preserves capital and maintains liquidity. The return is low because that’s the price of certainty. A savings vehicle answers one question: will this money be here when I need it?

Investing accepts uncertainty in exchange for expected growth over time — based on the fundamentals of a productive asset you understand. Time horizon matters. Analysis matters. The ability to hold through volatility without being forced to sell matters.

Speculating is a bet on price movement, narrative, or timing. You might be right. The return can be significant. But the logic is fundamentally different from investing — and the risks are different too. The danger isn’t speculation itself. It’s mislabeling speculation as investing and then behaving like an investor when you’re actually a speculator.

Gambling is pure chance with negative expected value over time. No productive asset underneath. No analysis that improves your edge. Just the hope that the outcome breaks your way.

Most retail participation in public markets — index funds included — sits closer to the speculating end of this spectrum than people are comfortable admitting.

Why Passive Doesn’t Mean Safe

The rise of index investing created a comforting story: you don’t need to pick stocks. Just own the whole market. Let compounding do the work.

That story isn’t wrong. But it obscures something important.

Buying an index fund without understanding what drives its returns is still a bet. You’re speculating that corporate profit margins will remain elevated, that valuation multiples won’t mean-revert, that monetary policy will remain supportive, and that you won’t need liquidity at exactly the wrong moment in the cycle.

Those are assumptions. Reasonable ones, historically. But assumptions nonetheless — not guarantees.

When roughly 60% of U.S. equity market volume is driven by algorithmic trading and passive index flows, price is increasingly disconnected from individual business fundamentals. You are not buying ownership stakes in productive businesses at a fair price. You are buying into a basket of prices set largely by machines and momentum.

That’s a bet on the continuation of flows. Not an investment in underlying value.

📖 Related: Artificial Wealth: When Prices Rise but Value Doesn’t — From 2009 to 2021, global M2 money supply and the S&P 500 grew at almost identical rates. Understanding what actually drove those returns matters enormously for what you should expect going forward.

The Incentive Structure Nobody Talks About

Here’s the other half of the problem.

Most people don’t arrive at their investment decisions independently. They arrive at them through a system of intermediaries — each of whom has their own incentives.

Financial media needs engagement. Fear and greed generate clicks. Balanced, nuanced analysis does not.

Advisors compensated on assets under management are paid to keep assets in the market. Moving to cash, reducing exposure, or recommending something outside the traditional portfolio isn’t in their fee structure.

Retirement plan providers need simplicity and scale. Target-date funds and default allocations are designed to minimize decisions — not to optimize outcomes for your specific situation, timeline, or risk tolerance.

None of these parties are necessarily acting in bad faith. But none of their incentives are aligned with the question you actually need to answer: does this capital structure serve my goals, under the conditions that will actually test it?

Most people outsource that question entirely. They follow the script — and call it a plan.

📖 Related: The Gap Between the Marketing & the Math — The most-read article on this site. The numbers your advisor shows you and the numbers that end up in your account are two very different figures.

Speculation Is Invisible Until It Isn’t

The deepest problem with speculation disguised as investing is that it’s undetectable in rising markets.

When prices climb year after year — when every dip is bought back, when the Fed reliably cuts rates before damage compounds, when the narrative of long-term investing always appears validated — speculation and genuine investing produce nearly identical outcomes.

Everyone feels smart. Everyone stays the course. Everyone’s plan looks like it’s working.

Speculation only reveals itself when markets turn. When volatility exposes who understood what they owned and why — and who was simply riding momentum on borrowed confidence.

That’s the moment people discover that their “investment portfolio” didn’t have the liquidity they assumed. That their timeline was shorter than their positions could accommodate. That they were positioned for appreciation, not for resilience.

📖 Related: When Liquidity Masquerades as Skill: The Rise of Entitled Investors — Fifteen years of policy-driven tailwinds trained a generation to believe the market owes them positive returns. The conditions that made that true may not last.

The Question Behind the Question

This article isn’t an argument against public markets. It’s not a case for abandoning equities or retreating to cash.

It’s an argument for honesty about what you’re doing and why.

Because the investor who knows they’re speculating can manage it accordingly — sizing positions appropriately, maintaining genuine liquidity elsewhere, building the structural redundancies that a speculative position doesn’t provide.

The investor who believes they’re investing — but is actually speculating — does none of that. They treat their speculative positions with the patience and conviction appropriate for long-term investments, and they’re exposed in exactly the scenarios that matter most.

True wealth isn’t built by pretending risk doesn’t exist. It’s built by understanding it — then designing around it intentionally.

If you want a framework for evaluating every dollar you own against the correct standard, The Capital Decision Filter is a free resource that walks you through exactly that exercise.

And if you’re ready to build a capital structure where some dollars are protected regardless of what public markets do — the team at Producers Wealth works specifically with business owners and high-income earners on building that system.

The Critical Thinking Three

- For every position in your portfolio, can you clearly articulate what you own, why you own it, what the underlying asset is worth, and at what price it becomes a bad decision? If you can’t, that position is speculation — regardless of how it’s labeled.

- What would happen to your financial plan if public markets produced flat or negative real returns for the next ten years? Not a crash — just a decade of sideways. Does your current structure still work? What breaks first?

- Who designed your current investment strategy — and what were their incentives when they did? How much of your current approach was built for your specific situation versus inherited from a default recommendation?

Not ready to talk yet? Join the Wealth & Liberty newsletter — one idea per week that challenges the default financial narrative and gives you a sharper framework for thinking about your own money.

When you’re ready for a real capital structure conversation, Producers Wealth is the place to start.