Imagine the stock market is a bowl of soup.

The soup itself represents real value — productive businesses, innovation, profits, human labor creating goods and services that people actually want. The bowl’s contents are what matter. The level is just how full it looks.

Now imagine the central bank walks over and starts pouring water into the bowl.

The level rises. The bowl looks fuller. From a distance, you’d think someone added more soup.

But nothing meaningful was added. The flavor is diluted. The nutrition is the same. The bowl didn’t get better — it just got more liquid.

That’s artificial wealth. Asset prices rising not because the underlying value increased, but because the number of currency units multiplied. The bowl looks fuller. What’s in it didn’t improve.

This is not a fringe theory. It is the most important lens for understanding what actually happened to asset prices from 2009 to 2021 — and what it means for the wealth you think you’ve built.

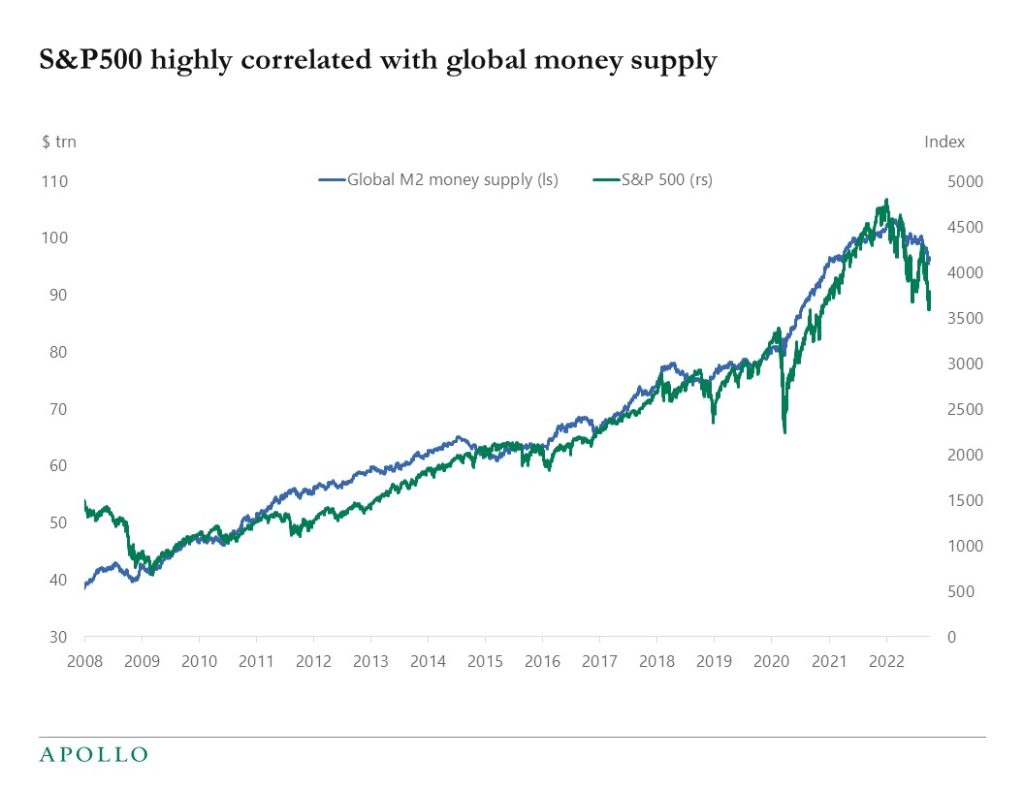

The Chart Nobody Shows You at the Advisor’s Office

Look at the S&P 500 and global money supply plotted on the same chart from 2009 to 2021. They move almost in lockstep. When money supply expands, asset prices rise. When liquidity tightens, markets wobble.

That correlation should force an uncomfortable question that most financial planning conversations are specifically designed to prevent:

Are markets rising because companies are creating dramatically more value — or because there’s simply more money chasing the same assets?

From 2009 to 2021, U.S. M2 money supply grew from roughly $8 trillion to over $21 trillion. The S&P 500 grew by approximately the same multiple over the same period. That is not a coincidence. It is the mechanism.

When you divide the S&P 500’s performance by the Federal Reserve’s balance sheet expansion over that period, a significant portion of the apparent gain disappears. What looked like wealth creation reveals itself as something closer to currency dilution denominated in rising nominal numbers.

The soup level rose. The soup didn’t improve.

📖 Related: When Liquidity Masquerades as Skill — Fifteen years of policy-driven tailwinds trained a generation of investors to believe their returns were a product of skill. The mechanism behind those returns tells a different story.

Why Artificial Wealth Feels Real

This is the part that makes the problem so persistent: on paper, artificial wealth looks identical to real wealth.

Your portfolio is up. Your net worth statement looks impressive. The account balance is higher than it’s ever been. The scoreboard is rising.

But quietly, simultaneously, the price of housing rose. Groceries cost more. Healthcare, education, and insurance all repriced upward. The dollar you’re measuring your wealth in is doing less work than it used to.

This is why so many people feel richer and more financially anxious at the same time. Both things are true. The number went up. The freedom that number represents didn’t grow at the same rate — and in some cases didn’t grow at all.

The investor who made 40% from 2020 to 2022 in a world where M2 money supply grew by $6 trillion and CPI ran at 8% didn’t necessarily improve their real claim on goods, services, and time. They may have run hard to stay in roughly the same place — like the Red Queen in Alice in Wonderland, running as fast as possible just to remain stationary.

Nominal gains and real gains are not the same thing. Most retirement projections and quarterly statements only show you the nominal number.

📖 Related: The Misrepresentation of the “Average Rate of Return” — Nominal return figures have a second layer of distortion beyond volatility drag. Inflation-adjusted, after-tax compound returns tell a very different story than the headline average.

The Mechanism: How Artificial Wealth Gets Created

The modern financial system distributes newly created money unevenly — and the sequence matters enormously for who benefits and who pays.

New money enters through banks and capital markets first. It bids up financial assets — stocks, bonds, real estate, private equity. Asset prices rise. Portfolio statements look good. Investors feel wealthy.

Then, with a lag, that expanded money supply bleeds into consumer prices. Groceries, rent, healthcare, energy. By the time inflation shows up at the checkout line, asset prices have already adjusted upward. The people who own financial assets got the benefit of rising prices before the cost of rising prices arrived. Everyone else — people holding cash, people renting rather than owning, people building savings in low-yield accounts — absorbs the purchasing power loss without having received the asset price gain first.

This is not an accident of the system. It is a feature of how monetary expansion distributes its effects. Those closest to the money creation benefit first. Those furthest from it absorb the dilution last.

Understanding this doesn’t make you cynical. It makes your financial planning more honest.

📖 Related: The 3 Forces Quietly Destroying Your Wealth — Inflation is one of three systematic forces eroding real purchasing power that most wealth plans never explicitly account for.

Artificial Wealth Is Fragile Wealth

Here’s the practical danger that flows from all of this.

Artificial wealth — wealth built primarily on monetary expansion and policy-driven asset price inflation — is structurally dependent on the continuation of the conditions that created it. It requires continued liquidity, accommodative interest rates, expanding credit, and sustained confidence in policy decisions you don’t control and cannot predict.

When those conditions change — when the water stops pouring into the bowl — valuations compress, volatility spikes, and liquidity vanishes precisely when it’s needed most. Not because the underlying businesses changed. Because the monetary environment that inflated their prices reversed.

This is what 2022 demonstrated. Interest rates rose. The Fed began contracting its balance sheet. Asset prices fell sharply — not because corporate fundamentals deteriorated in proportion to the price decline, but because the discount rate that had artificially elevated valuations for a decade was being normalized.

Investors who understood what had driven the gains could see this coming and position accordingly. Investors who believed the gains were entirely the product of business value creation were caught flat-footed.

The difference between those two groups wasn’t intelligence. It was the framework they used to evaluate what they owned.

📖 Related: A Nation of Speculators — Speculation disguised as investing is how wealth plans look great during the expansion phase and disappoint badly when conditions normalize.

What Real Wealth Actually Measures

The question Wealth & Liberty asks is never just “how high can prices go?”

It’s: how durable is this? How liquid is it under stress? How much of it depends on conditions continuing — and how much of it holds regardless?

Real wealth is measured not by the number on a statement but by what that number can actually do — the purchasing power it represents, the cash flow it generates, the optionality it provides, the stability it offers when the environment changes.

A rising soup level doesn’t mean you’re better fed. It means the bowl looks fuller.

The investors who navigate monetary cycles most effectively tend to have some capital in structures that don’t depend on policy tailwinds — assets that grow contractually rather than speculatively, that hold value because of what they are rather than because of the liquidity conditions surrounding them.

That’s not a retreat from growth. It’s a recognition that not all growth is the same kind, and that a capital structure built entirely on the continuation of one monetary regime is not a diversified plan. It’s a single concentrated bet dressed up as prudence.

If you want a framework for stress-testing how much of your current wealth is real versus policy-dependent, The Fragility Test is a free 10-minute diagnostic that asks exactly those questions.

And if you’re ready to explore what a capital structure looks like when some of your dollars are protected from monetary dilution entirely — the team at Producers Wealth builds exactly that.

📖 Related: Why Banks Love Life Insurance — The institutions that understand capital allocation best hold meaningful positions in assets that aren’t subject to the same monetary expansion dynamics that inflate and deflate market prices.

Not ready to talk yet? Join the Wealth & Liberty newsletter — one idea per week on building wealth that holds up under the conditions that actually test it.

The Critical Thinking Three

- If the money supply stopped expanding tomorrow, how much of your current portfolio value would still exist? This forces an honest separation between gains driven by real value creation and gains driven purely by liquidity and monetary expansion. Most investors have never run this thought experiment.

- What is your real inflation-adjusted, after-tax compound return over the last ten years — not the nominal figure your statements show, but what your purchasing power actually grew by? For most investors, this number is significantly more sobering than the headline return. The ones who’ve calculated it are rarely satisfied with what they find.

- How much of your net worth depends on markets staying calm, liquid, and policy-supported — and how much of it holds regardless of those conditions? At what point does a wealth plan built on favorable conditions become a bet on those conditions continuing rather than a genuinely resilient structure?