When Liquidity Masquerades as Skill: The Rise of Entitled Investors

For roughly fifteen years, almost every investor who stayed in the market made money.

Not because they were disciplined. Not because they were smart. Not because they picked the right companies, built the right systems, or understood something the market had missed.

Because the money supply expanded — relentlessly, deliberately, and at a scale history has no real precedent for.

From 2009 to 2021, the U.S. M2 money supply grew from roughly $8 trillion to over $21 trillion. The S&P 500 grew from roughly 666 to over 4,700. If you owned almost anything during that window and simply held it, you made money. And in making that money — easily, repeatedly, with every dip quickly reversed by policy — a generation of investors learned something that will cost them dearly in the next regime.

They learned that the market owes them a positive return.

That is the entitlement. And it is not a character flaw. It is a conditioned response — trained by fifteen years of evidence that says: if you just stay the course, the system will rescue you.

Understanding where that belief came from is the first step to building wealth that does not depend on it being true.

The Birth of a Conditioned Generation

The conditioning did not happen all at once. It was built, crisis by crisis, rescue by rescue, over more than two decades.

The dot-com collapse in 2000–2002 wiped out trillions in paper wealth. The Fed cut rates aggressively. Markets recovered. Lesson delivered: drawdowns are temporary. Policy responds.

The 2008 financial crisis was the most severe since the Great Depression. The Fed dropped rates to zero and launched an unprecedented quantitative easing program — buying Treasury bonds and mortgage-backed securities to inject liquidity directly into the financial system. Markets bottomed in March 2009 and began one of the longest bull runs in history. Lesson reinforced: even catastrophic crashes get reversed. Stay in.

COVID-19 in 2020 caused the fastest 30% market drawdown in history. Within weeks, the Fed had cut rates back to zero, announced unlimited QE, and Congress had passed the largest peacetime fiscal stimulus in American history. The market recovered to new all-time highs within five months. Lesson cemented: the government will not let the market fail. The floor is guaranteed.

Each rescue was faster and larger than the last. Each one trained the same reflex. Each one added another layer to what became — for millions of investors — a deeply held belief operating just below conscious awareness:

If I just stay the course, someone will fix it.

That belief is not investing. It is dependency.

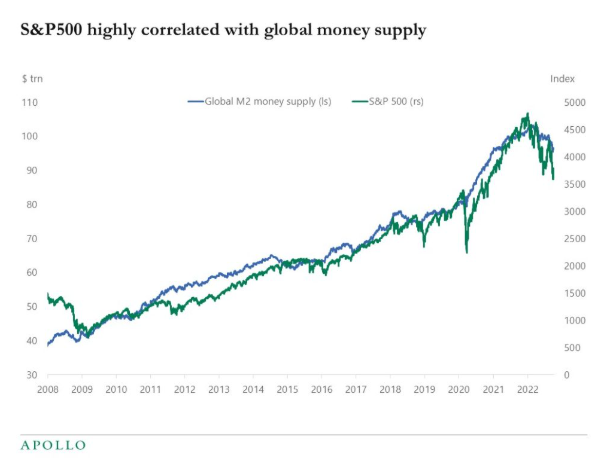

When Your Chart and the Money Printer Move Together

Here is the number that reframes everything.

From 2000 to the early 2020s, global M2 money supply grew at approximately 7.3% annually. Over the same period, the S&P 500 grew at approximately 7.1% annually.

Almost exactly the same line. For over twenty years.

This is not a coincidence. It is a relationship — and understanding it forces an uncomfortable question about what kind of return you actually earned.

When you divide the S&P 500 by the Federal Reserve’s balance sheet, a chart that looks like a surging bull market flattens dramatically. Much of the apparent gain disappears. What looked like wealth creation reveals itself as something closer to wealth re-denomination: the same real claims on goods, services, and productive capacity — just measured in a unit that has expanded significantly.

As we explored in Artificial Wealth: When Prices Rise But Value Doesn’t, asset price inflation and real wealth creation are not the same thing. A portfolio that doubles in a world where the money supply also doubles has not necessarily grown in any meaningful sense. The numbers are larger. The purchasing power claim may be roughly unchanged.

The honest question — the one almost no financial advisor will ask on your behalf — is this:

Did your portfolio grow? Or did your measuring stick shrink?

Generation Entitled Wealth is the cohort that mistakes asset price inflation for personal genius. That mistakes a liquidity-driven tailwind for investment skill. That mistakes policy support for market merit.

The confusion is understandable. The evidence pointed one way for fifteen years. But evidence from a manipulated environment is not the same as evidence from a market operating under normal conditions — and the regime can change.

What the Entitlement Sounds Like in Real Life

The mindset is not abstract. It has a voice. You have probably heard it — possibly in yourself.

“The Fed won’t let it crash too far.”

“This drawdown is temporary. They’ll pivot.”

“Just buy the dip. It always comes back.”

“Long-term investors always win. The data is clear.”

“If I just stay the course, I’ll be fine.”

None of these statements is purely wrong. Some version of each has been true for extended periods in U.S. market history. But embedded in each one is an assumption that deserves far more scrutiny than it typically receives: that the conditions which made it true in the past will continue indefinitely into the future.

That assumption is not an investment thesis. It is a bet on policy continuity.

It is a bet that central banks will always respond fast enough, with sufficient force, to prevent sustained drawdowns. That fiscal authorities will always be willing and able to backstop the financial system. That the dollar’s reserve status will remain unchallenged. That real rates will stay structurally low. That valuations can expand indefinitely without mean-reverting.

Those bets may pay off. They may not. But the investor who has never interrogated them — who holds them not as thesis but as assumption — is not managing risk. They are unaware of it.

As we examined in A Nation of Speculators, the dominant financial culture of the last generation optimized for return-chasing in favorable conditions and trained away the instinct for structural thinking. The result is a population of investors who are highly confident in environments that look like the last fifteen years — and deeply exposed in environments that do not.

Asset Price Inflation: Wealth or Mirage?

Low interest rates do something specific and mechanical to asset prices: they increase them, independent of underlying earnings or value creation.

When the rate used to discount future cash flows drops from 6% to 2%, the present value of every future dollar rises — automatically, mathematically, without any improvement in the actual business generating those dollars. This is not a market signal. It is a valuation artifact of monetary policy.

This means a significant portion of the equity gains from 2009 to 2021 were not driven by companies earning more, growing faster, or delivering more value to customers. They were driven by the denominator — the discount rate — falling. Rates went down. Present values went up. Investors recorded gains.

When rates rise — as they did sharply beginning in 2022 — the same mechanism runs in reverse. Present values compress. Asset prices fall. Not because anything changed in the underlying business. Because the measuring stick shifted.

The investors who understood this going into 2022 were not surprised. The investors who believed their portfolio gains reflected genuine value creation felt, in many cases, betrayed. That feeling — the sense that something that was supposed to go up had been taken from them — is the entitlement made visible.

Real wealth creation is not this fragile. A business that generates stable, growing cash flow from real customers does not reprice 40% because a central bank changes its rate target. A private contract with defined terms does not evaporate when duration risk reprices. A properly structured life insurance policy does not lose a third of its value in twelve months because bond yields moved.

As we explored in How Fees, Taxes, and Emotions Are Quietly Stealing 70% of Your Return Potential, the gap between gross market returns and what investors actually keep — after inflation, after taxes, after the behavior gap, after sequence-of-returns risk — is far larger than the headline numbers suggest. Layer on top of that the gap between nominal returns and real purchasing power, and the picture of what fifteen years of liquidity-driven gains actually delivered is considerably less impressive than most portfolios imply.

Why Entitled Wealth Is Fragile Wealth

The core problem is not that liquidity-driven gains are illegitimate. Capital allocated into rising markets during a liquidity expansion is real money — as long as it is managed with clear eyes about what drove the gains and what conditions are required to maintain them.

The problem is the mindset that develops when those gains are attributed to the wrong source.

If you believe your portfolio grew because you made good decisions, you will make the same decisions in the next regime. If you believe the market owes you positive returns because it has always delivered them, you will behave as if the current regime is permanent. You will stay fully invested through a valuation reset that could take years to resolve. You will decline to build the structural redundancies that durable wealth requires. You will remain dependent on policy heroics that may not arrive on your preferred timeline.

When you believe the market owes you a positive real return, you stop doing the hard work of building structures: cash-flow buffers, private contracts, uncorrelated assets, and systems that do not require permanent heroics from central banks.

Entitled wealth is fragile wealth because it is built on an assumption — policy continuity — rather than on a structure. It looks fine in normal conditions. It reveals its fragility in the moments that actually test a wealth plan: sustained drawdowns, liquidity crunches, rate regime changes, or simply the forced need to sell at the wrong time.

As we explored in Market Makers: How Wall Street Monetizes Your Every Trade, the public market system was not built to protect your long-term capital. It was built to generate volume, liquidity, and fee revenue for its intermediaries. The investor who mistakes participation in that system for ownership of a durable wealth structure is confusing the vehicle with the destination.

Free Resource: If you want to stress-test your own capital structure against the risks described in this article — conditional liquidity, policy dependency, and nominal vs. real return gaps — download The Fragility Test. It is a free diagnostic that takes 10 minutes and asks the questions most financial plans never do.

From Entitlement to Stewardship: What the Shift Looks Like

The antidote to entitled wealth is not pessimism. It is not abandoning public markets or predicting catastrophe.

It is precision.

It is asking, for every dollar of capital, what job that dollar is assigned to do — and whether the vehicle it sits in is actually designed to do that job under the conditions that matter most.

Families who build durable wealth across generations do not do so by riding liquidity cycles more skillfully than others. They do it by building structures whose function does not depend on any particular monetary regime. Cash-flow generating assets that produce income regardless of valuation multiples. Private contractual positions with defined terms that do not reprice when rates move. Liquidity reserves that are accessible without forced market timing. Legacy systems designed to transfer cleanly across generations without depending on sustained bull markets.

This is what the shift from entitlement to stewardship looks like in practice. Not a different set of tickers. A different set of questions.

Not: “What has performed best over the last fifteen years?”

But: “What still works if the next fifteen years look different from the last fifteen?”

Not: “How do I maximize return in a low-rate environment?”

But: “What parts of my capital structure function regardless of what rates do?”

As we examined in Why Family Offices Are Moving From Wall Street to Main Street, the most sophisticated capital allocators in the world are already asking these questions — and the answers are leading them away from total public market dependence and toward private, contractual, cash-flow-based structures that do not require sustained policy support to deliver on their function.

Free Resource: The Capital Decision Filter is a free framework for evaluating any financial decision against the criteria that durable wealth actually requires — not the criteria the last fifteen years trained you to use. Download it free.

Closing Reflection

The market did not fail Generation Entitled Wealth. The market performed exactly as markets do — responding to the most powerful monetary intervention in modern history with the asset price inflation that intervention was designed to produce.

The failure, where it exists, is in the interpretation. In mistaking a policy-driven tailwind for a permanent feature of the investment landscape. In building confidence, identity, and financial plans on conditions that were exceptional — and treating them as if they were normal.

The investors who will navigate the next regime most successfully are not the ones who predicted it earliest. They are the ones who built structures that do not require them to predict anything at all.

Structures that produce cash flow without depending on multiple expansion. Structures that maintain liquidity without requiring favorable market conditions. Structures that transfer cleanly across generations without depending on what the Fed decides to do in the decade your heirs inherit.

The question is not whether the next fifteen years will look like the last fifteen. The question is whether your wealth plan still works if they do not.

If that question deserves a serious answer, the team at Producers Wealth builds capital structures for business owners and high-income earners who want their system to function regardless of what monetary policy does next. Start the conversation.

The Critical Thinking Three

The Critical Thinking Three

- If central banks stopped backstopping markets tomorrow — no more QE, no emergency rate cuts, no “whatever it takes” — how much of your portfolio’s performance over the last fifteen years would you still consider the result of sound decisions rather than favorable conditions you did not control?

- Are you measuring your investment success in nominal returns, or in real purchasing power and control? When you account for inflation, taxes, fee drag, and the behavior gap, what did your portfolio actually earn in terms of what it can buy — and what it allows you to do?

- What parts of your current wealth plan still function if liquidity tightens, valuations reset, and the “the Fed will fix it” assumption proves wrong for a decade? Which of your structures depends on rescue — and which one operates regardless of whether rescue arrives?

The last fifteen years trained a generation to believe that staying in the market was the same as building real wealth. For much of that period, it was close enough to true that the distinction did not matter. The distinction is beginning to matter. If you want to explore what wealth looks like when it is built for regimes that do not require rescue, start that conversation with Producers Wealth.